The Future of Staking: A Look at Ethereum's Shanghai Upgrade

The Ethereum ecosystem is on the brink of a significant transformation with the upcoming Shanghai upgrade. This article explores key metrics and delves into the potential impact of the hard fork on the staking ecosystem.

The highly anticipated Shanghai upgrade is just around the corner, with testing efforts on Goerli scheduled for March 14th and Mainnet launch estimated for the second week of April. Shanghai represents a major landmark for the Ethereum ecosystem, allowing withdrawals from staking contracts for the first time.

This event offers the first chance for a complete reset of the staking industry. Up until today, market participants have faced challenges in efficiently transitioning between staking products due to a deferred reward mechanism. Withdrawals provide the freedom to switch products freely, thereby enabling users to take a break from validating, try out a new service, or find enough confidence to run a node themselves. The reduced friction brought by withdrawals will serve as the driving force behind the next transformation of the Ethereum staking market.

General consensus is that withdrawals will significantly lower the risk associated with Ethereum staking, making it a more viable alternative for a broader range of institutions and investors. Until now, the absence of withdrawals has hindered access to a global stockpile of one the world's most valuable assets worth around ~$29B. Soon, staking rewards will be available to be accessed and streamed immutably for a variety of actions, including donating and funding public goods. Enabling withdrawals is also a critical step in the evolution of Ethereum's microeconomics. For the at-home validator, withdrawals enable a much-needed cashflow stream to fund operations (and maybe more!).

On this backdrop, below we present a series of key metrics we are following as we head into Shanghai, why they are relevant, and how they might change pre/post-Shanghai. The unclogging of Ethereum's circular value flow will likely serve as a major catalyst for the network's next chapter of growth and global adoption. As Dune says, the data must flow… in this case, it is time for Ether to flow.

Participation Rate

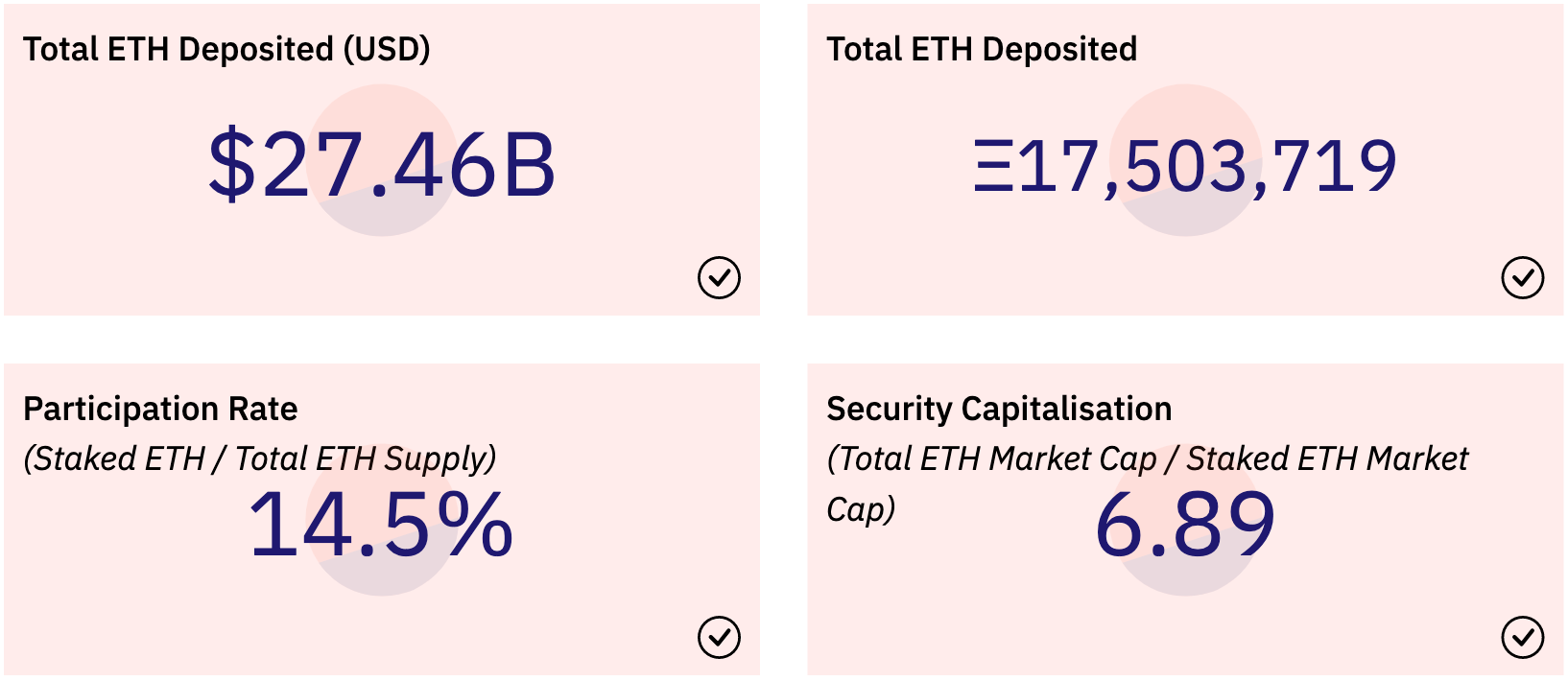

To date, over 17.5M ETH has been staked on the Beacon Chain since it went live in 2020, steadily increasing at a month-over-month rate of 13.4% (~546k validators securing the chain at the moment). With ~120.5M ETH currently in circulation, the network’s participation rate stands at 14.5%. However, since The Merge, the MoM growth rate for deposits has decreased to an average of 4%, indicating a certain decrease in appetite for running validators.

Post Shanghai, the decrease in risk is expected to drive a substantial increase in the participation rate, potentially doubling in value. Ethereum researcher Justin Drake pointed towards this direction back in 2019, stating that ~33.5M ETH would be reasonable for the network’s security (to reach this security threshold, current staked ETH deposits would need to approximately double).

However, despite the enabling of withdrawals, there are some valid concerns about staking participation effectively declining, given that annualised staking rewards for validators are currently lower than more stable options such as US Treasury bills.

Finding Balance

More interestingly, what Shanghai will enable is for the Ethereum reward rate to move closer to true market equilibrium. It is the first time the rate can functionally move higher, creating the two-sided market we need to mature staking. Not only will it incentivize more stake, but it will also enable exits for those who would like to move on to something new, an event that would increase validator rewards (i.e: decreasing the validator count would effectively increase yield for stakers).

While it's expected that participation rates will likely double or more with the introduction of withdrawals, it's unlikely that the total participation will reach equilibrium levels similar to those seen on other PoS chains, which often have participation rates of over 60% of the circulating supply or more. Such a high participation rate would result in lower staking rewards, potentially making it unappealing for validators to participate (with 60% of circulating supply staked - ~72M ETH - net annualised return for an average Ethereum validator would stand at ~0.86%). Thus, it's unlikely that economic incentives alone would be sufficient to sustain such a high participation rate.

Additionally, Ether's widespread use as a medium of exchange could further limit the participation rate. The use of Ether as a currency means that many token holders may not be interested in staking their coins, as they might prefer using them for other purposes, such as trading, investing, or transacting. So even if economic incentives for staking were more attractive, the overall participation rate may still be limited by the number of token holders unwilling to lock up their coins for a prolonged period of time.

We calculate the Participation Rate ratio as:

Participation Rate = Staked ETH / Total ETH Supply

The main reason why this metric is important to follow is that Ethereum validator economics are inversely correlated with the number of active validators. In other words, as the participation rate decreases, the reward for network validators increases. This dynamic has a ripple effect throughout the network. Large swings in this metric can be attributed to the most fundamental validator behaviour, which are validator entry and exit patterns. We view this as a crucial macro metric that has trickle-down effects on the rest of the action.

We also envision the participation rate as a security-denominated multiple, called Security Capitalisation, where:

Security Capitalisation = Total ETH Market Cap / Staked ETH Market Cap

This metric represents the amount of economic security being provided to the network compared to the total market value of the network. In a case where the multiple is too high, then speculation will exceed the network security, and vice versa.

With the current ETH market capitalisation, Security Capitalisation stands at ~6.89x, showing a 94.5% drawdown since its maximum recorded value back in December 2020, where the multiple topped out at 125.5x.

Historically, security capitalisation has been steadily decreasing MoM, with speculation diminishing significantly as the crypto market matures and Ethereum network security approaches a reasonable threshold (see here). It will be exciting to watch this metric mature as chain security stabilises post-Shanghai.

Where Will Ethereum Stake Go?

Building on the total participation rate, we are closely following where stake deposits land once they enter or exit the network. Following Shanghai, the topography of network stake will have the opportunity to morph adapting to different market realities, a substantially different landscape than when we launched the Beacon Chain.

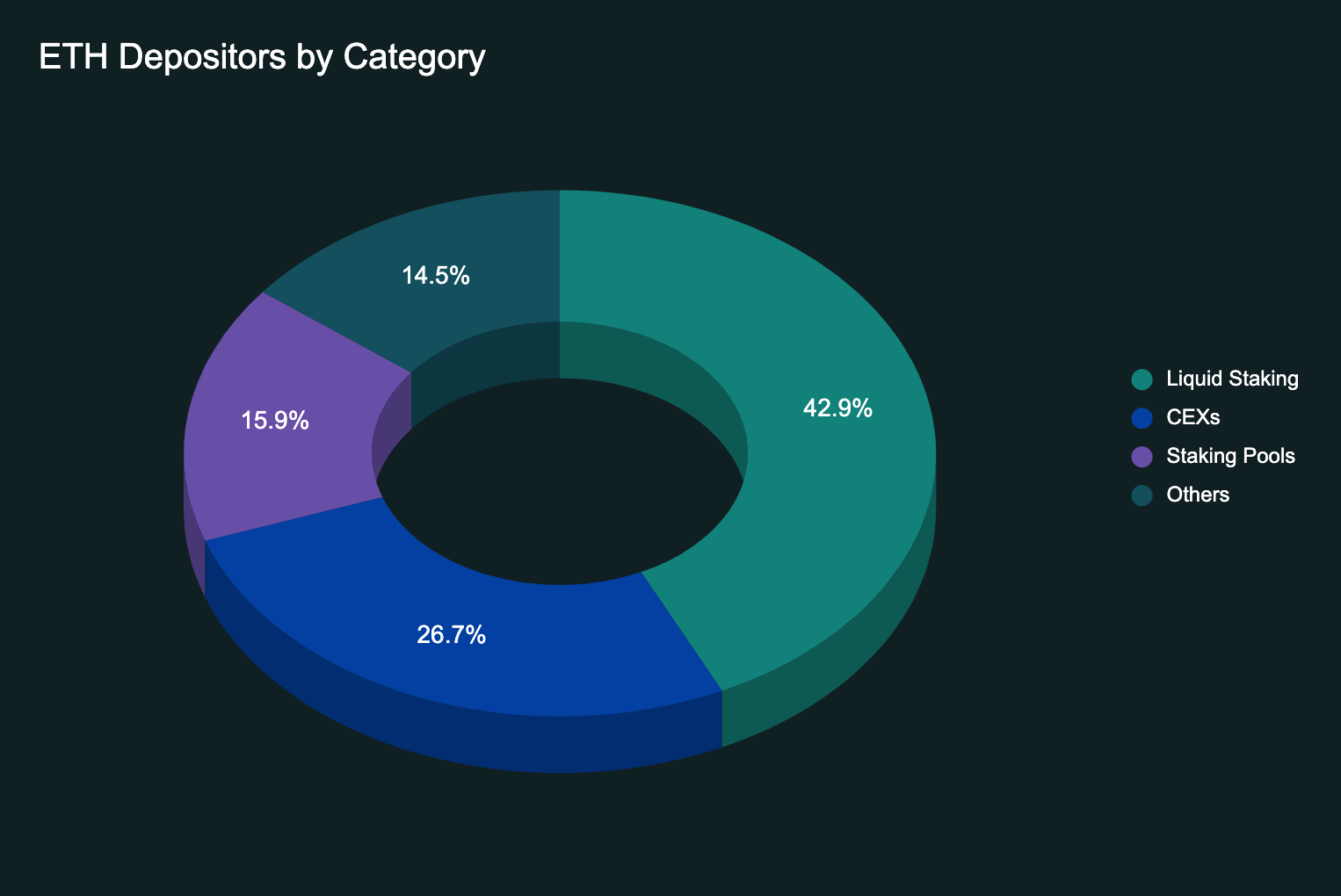

As we can see depicted in the graph above, at the moment liquid staking protocols hold the biggest share of the market, standing at ~43%¹ of ETH staked, with Centralised Exchanges following closely behind. Liquid staking protocols at the moment represent a ~$11.5B market that has been consistently growing over the past years, with an average MoM growth rate of 28.2%.

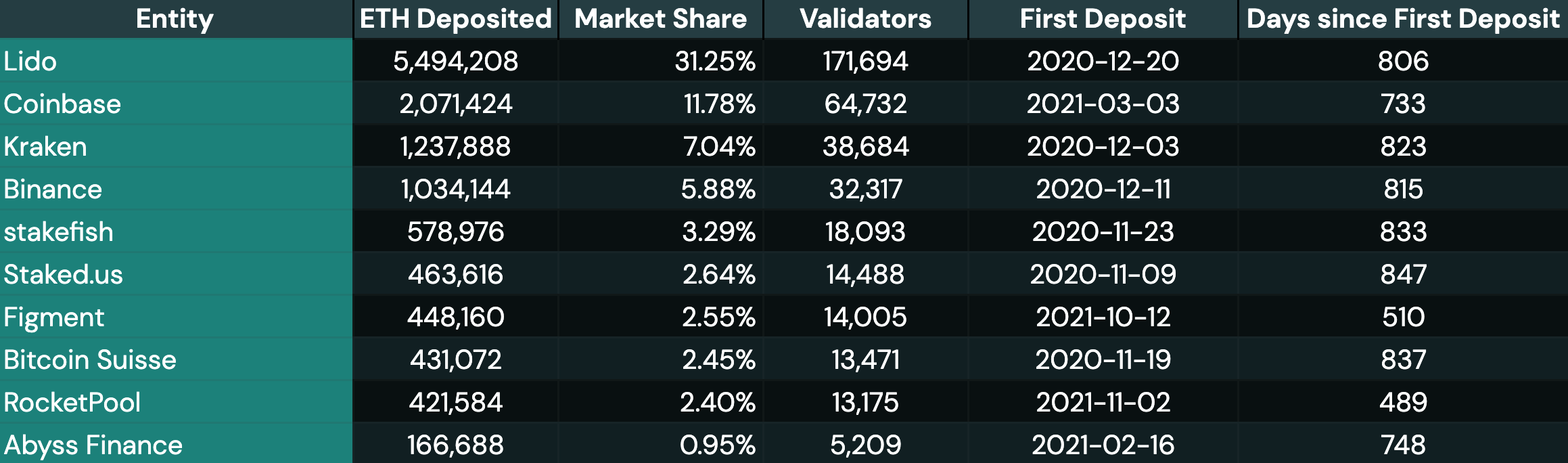

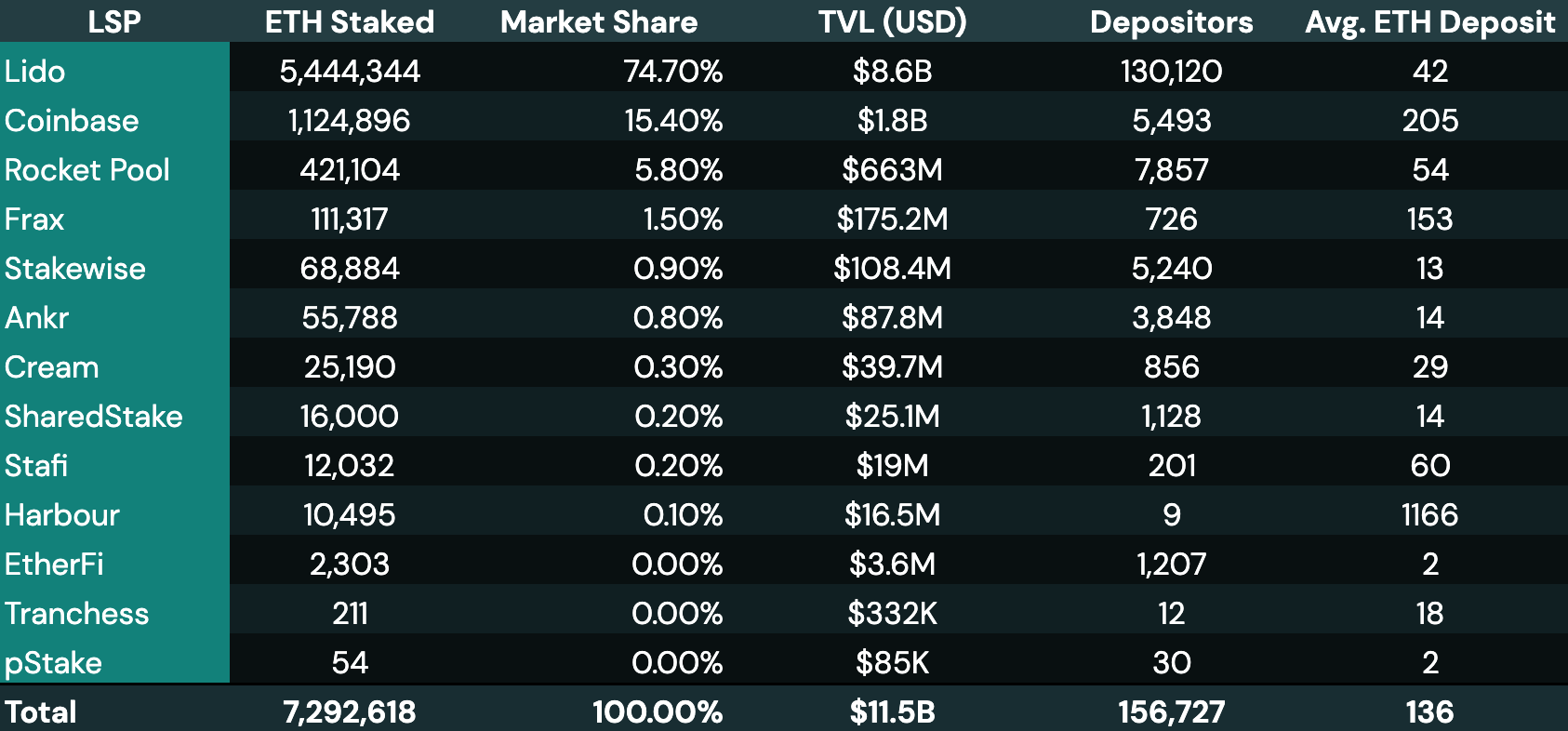

As the table below illustrates, a significant portion of the total ETH staked is held by just four entities - Lido, Coinbase, Kraken, and Binance - accounting for a staggering 56% of total ETH staking deposits. By comparison, an equivalent amount of staked ATOM on the Cosmos Hub is distributed across 18 validator entities.

The question of centralisation vs. decentralisation of stake is one that has been hotly debated in the Ethereum community. When it comes to the case for centralisation of stake, there are still several technical barriers that make it difficult for the average person to run a validator node. While centralised entities have made staking more accessible for non-technical users, further efforts are needed to decentralise staking operations in order to improve the health of the network.

The fear of slashing and downtime penalties still runs high for people staking their tokens, despite the fact that the number of validators slashed is still relatively low (only 229 validators slashed from over +546k validators). Secondarily, the monetary requirements (32 ETH / ~$50k) needed to operate a single validator force many people to rely on staking providers, leading to a natural pooling effect that exacerbates existing stake centralisation risk.

Currently, there are strong efforts underway to facilitate decentralisation of stake, with a very strong case being made for DVT leading this effort. A few benefits of DVT include:

- Increased Participation: By reducing the barriers to entry for running validator nodes, DVT encourages more people to participate in staking, leading to a more diverse and representative network. DVT allows smaller validators to deliver uptime and efficiency that is comparable to larger validators. The ETH requirement for running a node is also lowered, as multiple nodes can be grouped together to meet the 32 ETH (~$50k) requirement for validation.

- Decentralisation: DVT enables the decentralisation of the validation process by enabling a construct known as multi-operator validation, where the validator duties are split amongst a group of entities/individuals.

- Security: Multi-operator validation brings the risk of a single point of failure to nearly zero, significantly improving the overall security of the network.

- Improved ROI: By improving uptime and reducing slashing risk, DVT allows stakers to optimise their staking APR.

- Flexibility: DVT allows validator nodes to be run with different configurations, clients, locations, and organisations. This provides greater flexibility for staking and improves Ethereum's client diversity.

In-depth guides and general education on staking are also helping to reduce technical barriers. Plug-and-stake hardware is gaining traction, with projects like Dappnode and Avado leading the way. These efforts have the potential to make staking more accessible to a wider range of users and increase network node count, thereby improving decentralisation.

Liquid staking protocols are also transitioning into more decentralised specifications. Rocket Pool, Stakewise V3, Lido V2, are all examples of liquid staking models embracing a modular approach, where the user has increased decision power over how validator nodes are set up, and with DVT as a central element in the design of these specs.

Ultimately, the question of centralisation versus decentralisation of stake will likely continue to be a subject of debate. While technical barriers and the prevalence of staking-as-a-service providers have made centralisation a harsh reality for Ethereum, the introduction of DVT, a fresh legal paradigm, and increased efforts to improve accessibility/promote decentralisation will lead to a more democratic and secure network in the long run. It is important for users and stakeholders to carefully consider the trade-offs involved with each staking method and to strive for a balanced and sustainable approach to staking.

Liquid Staking

Monitoring the flow of ether into liquid staking pools is another significant area of focus, both on an individual and aggregate basis. As discussed in the previous section, liquid staking currently holds the biggest portion of the staking market, and it is poised for further growth given its lean business model that allows for efficient staking while reducing the high opportunity cost stakers face when delegating their tokens.

The purpose of liquid staking is to address the liquidity limitations of traditional staking methods. It was primarily designed to tackle Ethereum's liquidity limitation, where users have been unable to withdraw their funds since the Beacon Chain launched. We believe that liquid staking is an essential component of a mature market, as it allows universal access to staking in the most straightforward manner possible.

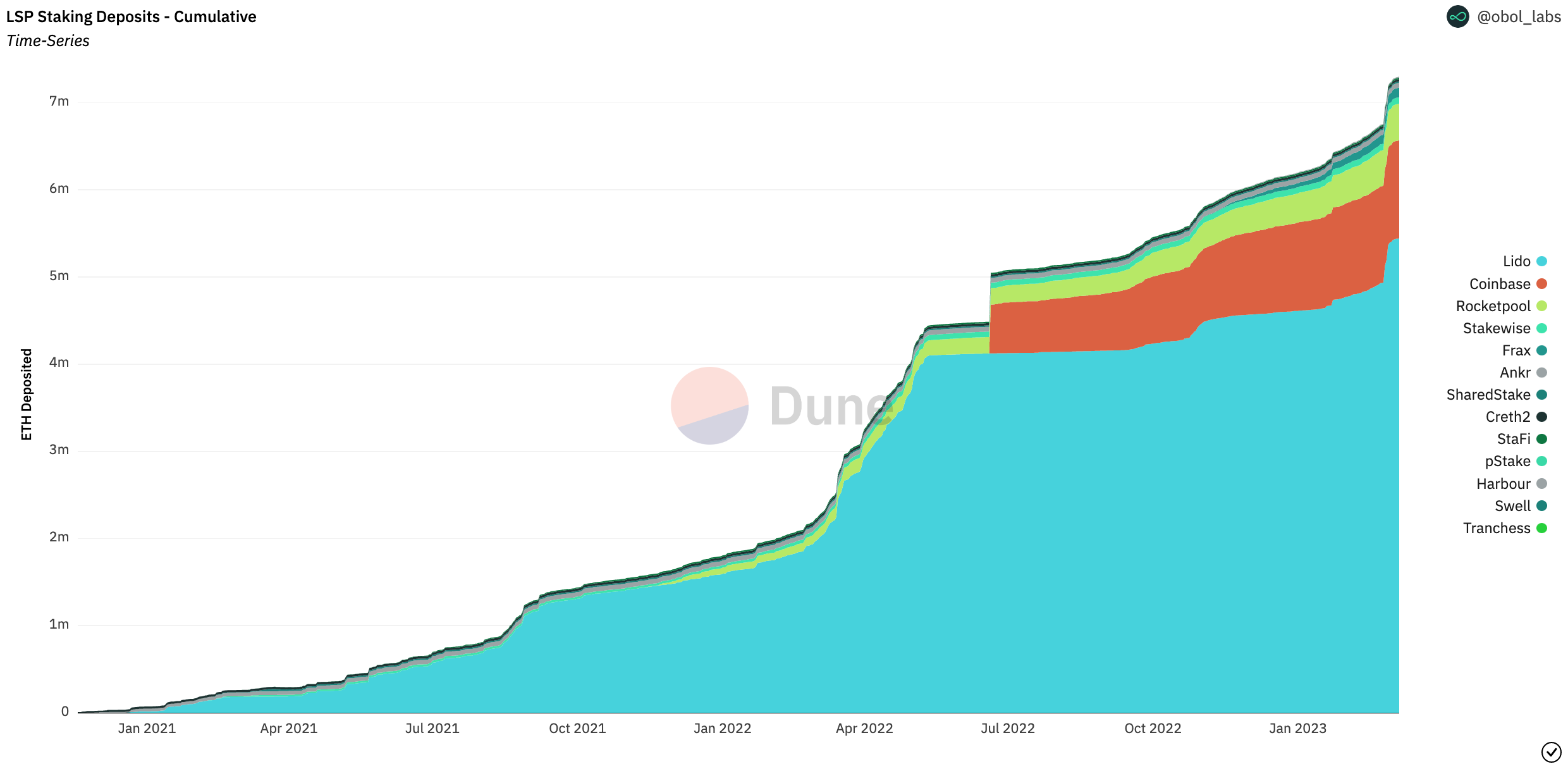

Despite its current market dominance, Lido is facing stiff competition from liquid staking protocols such as Rocket Pool, StakeWise, and Frax, which are slowly catching up to Lido’s market dominance. Furthermore, the entry of Coinbase (cbETH), one of the leading centralised exchanges and a major player in the industry, has intensified the competition even further. With its strong brand and reputation, Coinbase is well-positioned to onboard a significant number of stakers, and its impact is already being felt as it currently holds 15.4% of the liquid staking market.

The growth of cbETH has skyrocketed to approximately 1.1M as of March 6th, 2023. Meanwhile, Frax, which launched its liquid staking product in October, has seen very rapid growth thanks to its unique design that boasts the best APR in the market and now holds around 111k staked ETH as of March 6th.

The table below displays the top LSPs for Ethereum, with Lido leading the pack at 74.7% market share, followed closely by Coinbase at 15.4%, and Rocket Pool rounding out the top three with 5.8%. As we get closer to withdrawals, new market entrants will be hitting the market. Players such as Alluvial, with their institutional liquid staking solution, as well as Stader Labs and Swell are expected to deploy their products close to the Shanghai upgrade. EtherFi is also a key player to follow as the liquid staking market evolves.

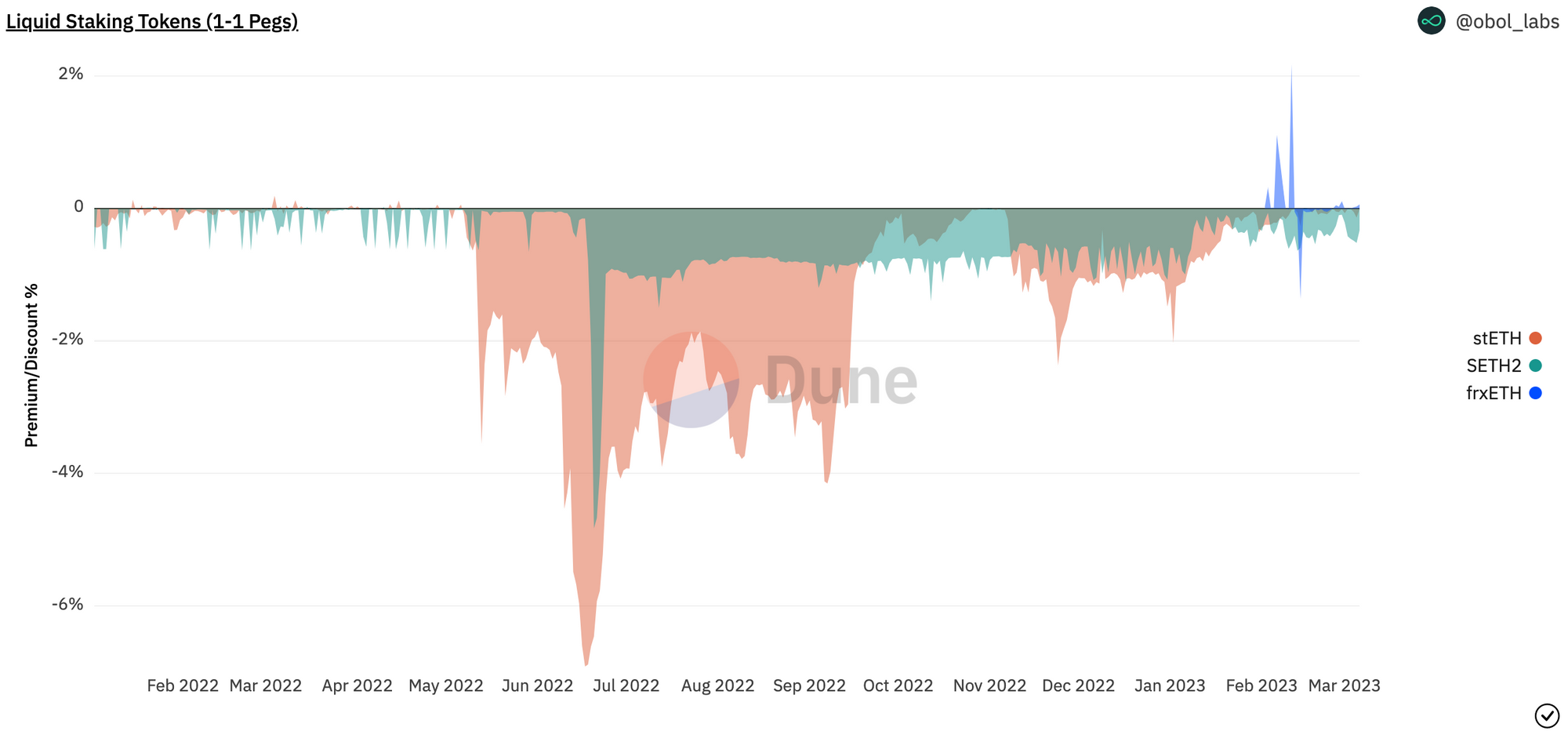

The main trend that has been observed in the liquid staking market is that most liquid staking tokens consistently trade at discounts to their underlying value. This phenomenon can be attributed to a variety of factors, including market volatility, liquidity constraints, and deficiencies given their deferred cash flows. In the past year, we have seen several significant sell-offs in the liquid staking market, including the LUNA collapse in May, the 3AC meltdown in June, and the FTX downfall in November.

Now that validator cash flows have become perpetual, the question remains whether LSTs will trade at premiums or discounts. Pre-withdrawals prices have been held together by incentivized liquidity and have been facing strong headwinds due to their structural deferred cash flows. Now that people are getting their ETH back, it will be a point of inflection for the future trading of LSTs. However, it is expected that the entry delay will be weeks long, forcing heavyweight capital players to quickly move into LSTs, pushing prices into premium territory. In addition, traditional financial theory would suggest that a validator should be more than 32 ETH as it has a reward stream attached to it. Yes, this is the dawn of a new era!

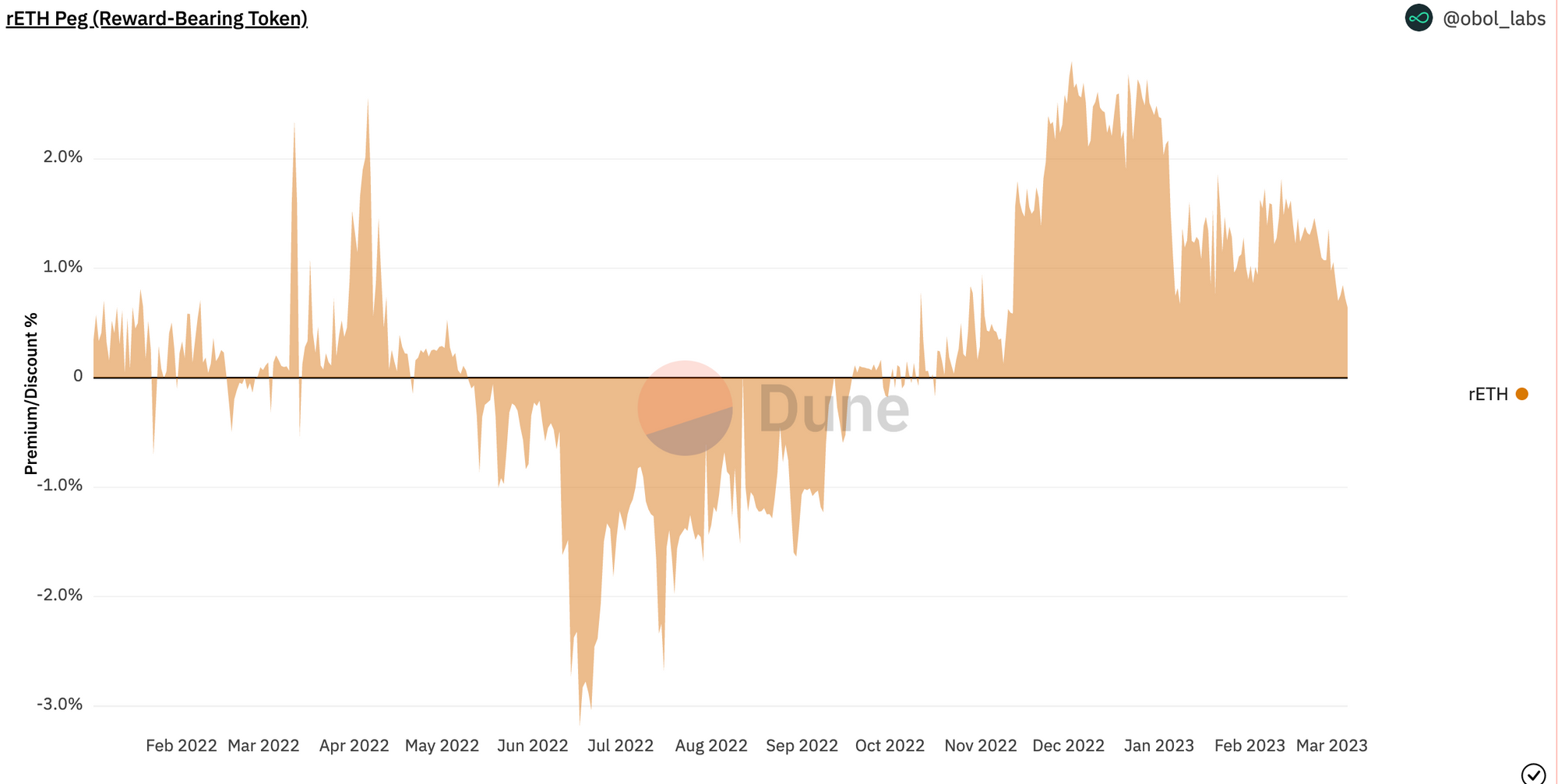

A clear outlier, however, is Rocket Pool. Rocket Pool’s rETH is consistently trading at a premium. This is primarily due to a push for more decentralised alternatives and due to the mechanism design of Rocketpool. rETH supply is correlated with node operator growth. As Rocket Pool has a widely distributed set of node operators, and there is currently a lack of demand for them to run mini-pool nodes, they currently have a significant chunk of ETH waiting in the deposit pool to be paired with mini-pool validators. As there aren’t enough mini-pool validators to take in the demand for deposits, this drives rETH to be trading at a premium.

The charts below distinguish between liquid staking tokens that are supposed to trade at parity with ETH 1-to-1 vs. reward-bearing tokens that increase in value relative to ETH. Reward-bearing tokens premium/discount is derived from the conversion rate, which in turn produces an implied fair value rate².

The turbulence caused by the downfalls of Luna and 3AC had a significant impact on all LSTs, driving them to trade at heavy discounts for a significant portion of 2022. Lido's stETH traded at a discount for most of the year, particularly between May and August, with an average discount of -1.42%. However, it has since recovered and is now trading close to its peg. Stakewise's sETH2 also struggled to maintain parity over the past year but has recently recovered and is now trading close to par. In contrast, frxETH has remained quite consistent since its launch in October, with few deviations from the peg except for a few outliers.

RocketPool had been trading at a premium until May when Luna collapsed. Like most LSTs, it traded heavily discounted until October, when it started to recover ground. Currently, it is back to trading at a premium, with an average of +1.78% above its implied fair value rate since October 2022.

ETH Inflation

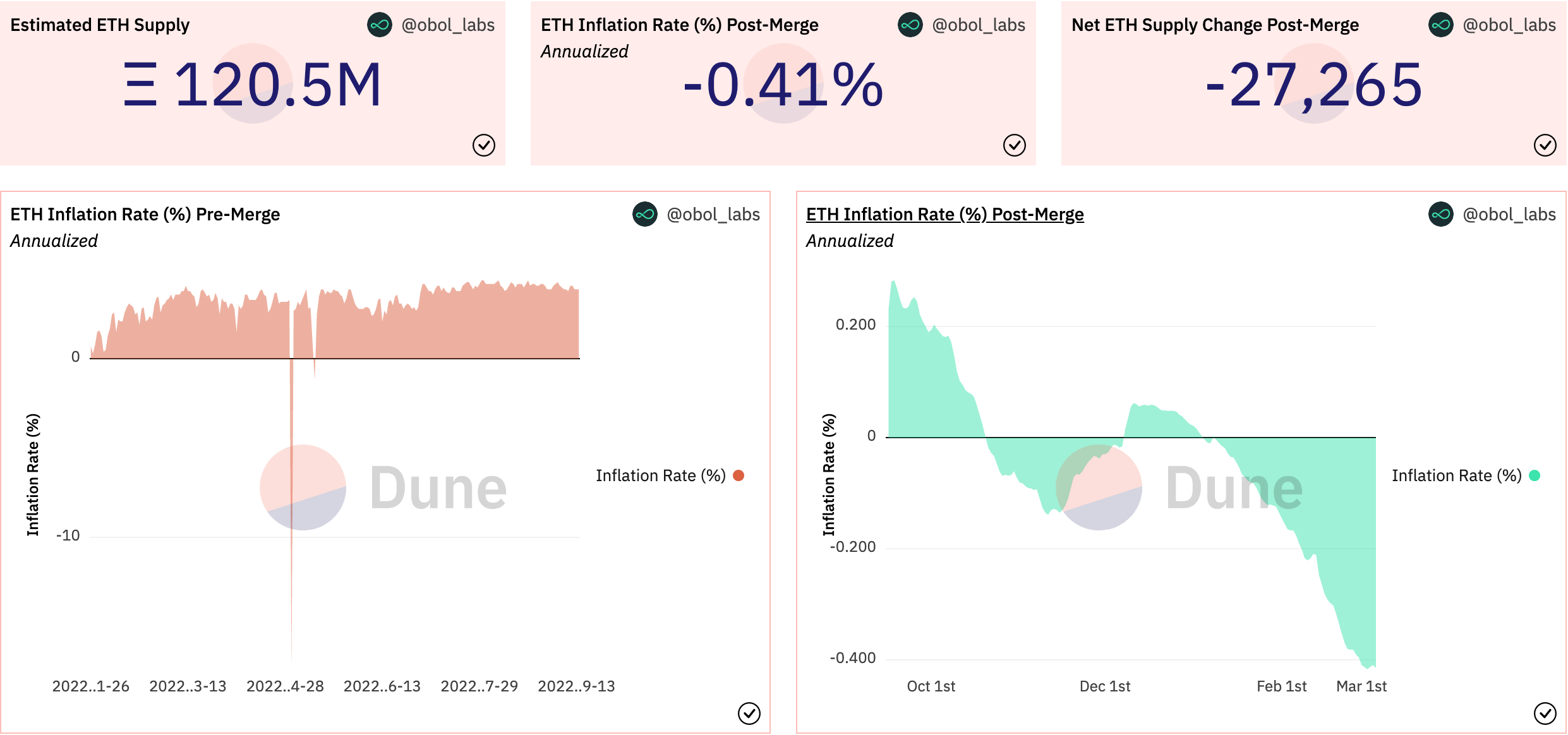

To wrap up our report, we'd like to touch on ether inflation. The transition from Proof-of-Work (PoW) to Proof-of-Stake (PoS) in September 2022 has resulted in ETH trending towards a deflationary state, with zero issuance on its execution layer, a concept referred to in the community as Ultrasound Money.

This has brought about a significant decrease in inflation compared to previous years. In 2022, ETH's inflation rate averaged around ~4%. However, post-merge, the annualised inflation rate stands at an impressive -0.41%, with ETH’s circulating supply effectively decreasing ~27.3k ETH, a 0.023% reduction since The Merge.

Transactions on Ethereum require a base fee paid in ETH for the transaction to be considered valid (see Ethereum EIP 1559). The fee is burnt during the transaction process, removing ETH from circulation. Fee burning went live with the London upgrade in August 2021 and remains unchanged since.

More simply put, as more people use the Ethereum Mainnet for transactions, more ether will be burned to cover transaction fees. This results in deflationary pressure on the supply of ether, which can be especially pronounced during significant on-chain events like NFT drops or market sell-offs.

The ETH Inflation Rate surrounding the Shanghai upgrade could experience a significant downward spike for a variety of reasons, but mostly due to the opportunity of withdrawals, which allows for ~$29B³ of validator balance to be moved around on-chain in a permissionless manner.

When that balance effectively hits the market, a large number of on-chain transactions will occur, leading to a substantial fee burn. Additionally, due to the low price of ecosystem assets, validators may directly swap their ETH for other blue chip tokens. This could result in a sharp decrease in inflation, similar to the spike observed with the Otherside Mint (BAYC) on May 1st, 2022.

However, validator balance will not flood the market all at once. The Ethereum spec limits the number of partial withdrawals to 256 per epoch (partial withdrawals are the ability to withdraw any balance above the 32 ETH of the validator, also known as staking rewards). This means that 57,600 partial withdrawals can be processed on any given day. With the current number of validators (~546k), if all of them wanted to withdraw partially, it would take ~9.48 days, resulting in a rewards dump that could stretch for a few days. For validators wanting to exit the validator set, WestieCapital from Blockworks Research put together a useful chart portraying how long the withdrawal waiting period would last depending on the percentage of validators wanting to exit the validator set at a given time.

Closing Remarks

The upcoming Shanghai upgrade of Ethereum will mark a major milestone in the network’s roadmap and an integral reset for the staking industry. With withdrawals, market participants will be able to freely switch staking products, and this reduced friction will transform the staking market landscape. Withdrawals will also significantly diminish the risks associated with Ethereum staking, onboarding the next wave of investors and institutions.

General de-risking of Ethereum will increase the participation rate in the network, as staking becomes the risk-free rate for the cryptocurrency market that enables people to actively participate in securing public blockchain networks.

At Obol, we will be headed to market as part of the greater Shanghai infrastructure transition in order to help secure validators in preparation for the increasing amount of ether being staked into the network. The deployment of Distributed Validator Technology (DVT) will further de-risk Ethereum staking by bringing validator slashing risk to virtually zero while providing highly available validators for the industry (Obol Labs launched the first ever distributed validator (DV) cluster on Ethereum mainnet on Dec. 30th, 2022 - more details here).

Decentralised and modular specifications will position liquid staking as the driving force behind the next wave of the staking industry, with the likes of Lido V2, Stakewise V3, and Rocket Pool. By giving stakers greater control over node operation, liquid staking will promote decentralisation while empowering users to participate actively in the network. As this segment continues to evolve and mature, we can expect to see even greater adoption and innovation in the staking space.

As the Ethereum community moves forward, we must strive to support the efforts being made to increase the network’s security and resilience. The deployment of DVT in conjunction with the rollout of withdrawals will make staking a fresh and productive ecosystem, with all the necessary elements to thrive and grow in a healthy manner.

As we approach the Shanghai/Capella upgrade, we invite you to check out our Dune ETH Staking Ecosystem dashboard for additional key insights - here.

Special thanks to @hildobby @eliasimos @LidoFinance @BlockworksRes @rp_community for publishing open-source queries that contributed to the making of this dashboard and report.

Notes:

- Beacon chain depositors' market shares are approximate, as not all addresses are available for matching against the different entities.

- The calculation for reward-bearing tokens derives from the following inputs: ETH/rETH Conversion Rate → Implied rETH Fair Value → Actual rETH value → rETH premium/discount

- Calculated as Average Validator Balance x No. of Active Validators x ETH Price ($1,560) as of Mar. 6th.